January feels like a month that can be quite dreary or ho-hum. Many of us have started with New Year’s resolutions, only to find we aren’t sticking to them like we’d like while, others of us had the hope that the flip of the calendar page to 2023 would make everything seem a bit different and better. Here in Alberta, we are in the middle of winter and, along with most of Canada, are finding the days too short, though getting longer, and the sun too limited. This isn’t painting the rosiest picture of January.

However, with all that Eeyore ho-humming, there is still a bright side! Give yourself some grace, a bit of a break, if you haven’t achieved that New Year’s resolution like you’ve hoped, dreamed or expected. One day at a time! To be very cliché, we can be the difference we were hoping for in 2023. Sometimes a perspective shift is all that’s needed to happen for things to improve. We can’t do anything about the weather, but make the most of those sunny days, sunrises and sunsets. Wow, I’ve waxed poetic from one extreme to the other here!

Here at Agfinity we don’t have any crystal balls or magic wands, believe me, we know how beneficial it would be if we did, but we are here for you to assist with all your resolutions, hopes and expectations for your grain marketing needs this 2023 and forward. We’d love to be able to wave our magic wands and get you the exact price you need or want or look into our crystal ball and say when the perfect time to market is, but as I let the secret out of the bag earlier, we don’t have either of those yet . . . Amazon just isn’t stocking them! We are here to provide you with the most up-to-date market information and pricing we can as a trading team to help you make the best decisions for you. Our CEC team is here to assist with meeting the movement needs for your marketed loads. So, give us a call and let us know what you are looking to sell or buy. We will work to provide you with the best grain trading opportunity.

We can’t make the sunshine, but we are here with a smile on the other end of the phone to chat. We are almost through January, however you felt about it, and are moving on to longer days, changing markets and before we know it springtime and seeding. We are looking forward to working with you this year!

Because Farming is Forever

Amy Billett

Market Report – Joseph Billett

We are seeing lots of grain offers being posted, however the spread between the seller and buyer is quite vast right now. With markets highs coming off and demand steady but not desperate, sellers are beginning to shift from greed to hope. If markets continue with this bearish tone hope may change to fear. Many sellers are in a “wait for the markets to rebound” state. For feed grains buyers are still seeing corn come into feedlot alley and can buy bits and pieces to cover their needs without needing to overpay or chase too hard. February is close to covered and March – April – May will be the opportunity for sellers but the preverbal ship may sale if procrastination has taken a hold of the sellers’ marketing decisions.

Wheat and Corn are seeing marginal rebounds over the past couple of days, making up most of Monday’s losses yesterday and so far today. Nearby Minnie Spring Wheat futures are up 21 cents per bushel over the past two day at $9.09/bu. The gains yesterday were largely about the changing forecast in the Southern Plains of the US which saw disappointing rain and snowfall totals in the region. The wheat market continues to be plagued by complacency, especially given the Russian invasion of Ukraine continues to rage on.

Chicago corn futures are managing to hold steady to a penny higher this morning after rallying 5 to 10 cents yesterday but may struggle to keep the gains. The corn market is inching its way back towards last week’s highs even as Argentina sees more desperately needed rain in near-term forecasts. USDA reported a private export sale announcement of 130,000 tonnes of US corn sold to unknown destinations for old crop delivery today. The pace of US corn exports overall this marketing year have been underwhelming so far, but the trade is looking for better US export potential between now and July when the second Brazilian corn harvest comes available to the marketplace. US domestic corn cash basis remains at its strongest in 20 years, a reflection of active demand for US ethanol and domestic feed needs.

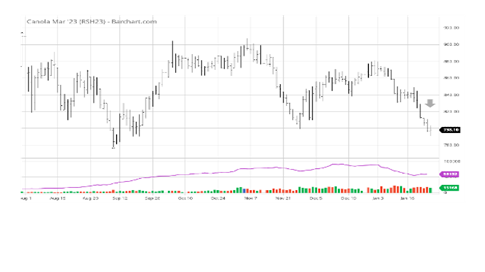

Speculative fund trading continues to pressure canola with the March contract dropping for five consecutive sessions, seeing a slight glimmer of life today. The trading pattern is very similar to the massive selloff in late November. The fundamentals are largely unchanged for canola, but the drop of C$10 per tonne yesterday in the March contract pushed canola to the lowest level since September 20th. Today, crude oil futures pressured the oilseed complex with nearby soybean oil futures dropping 1.7 per cent. Despite the drop in soybean oil futures, the canola crush margin for March remains high at C$227.21 per tonne. One of the factors in the vegetable oil markets this week is the Asian New Year holidays, which has closed down halted Malaysian palm oil futures. When the Asian buyers return to the market, analysts anticipate canola to rebound like it did in December.